- Auto-enrolment.

Create your own single employee experience.

With Auto-Enrolment (AE) legislation due to commence in January 2026, your immediate priority is to ensure your business operates one robust pension solution for all of your employees.

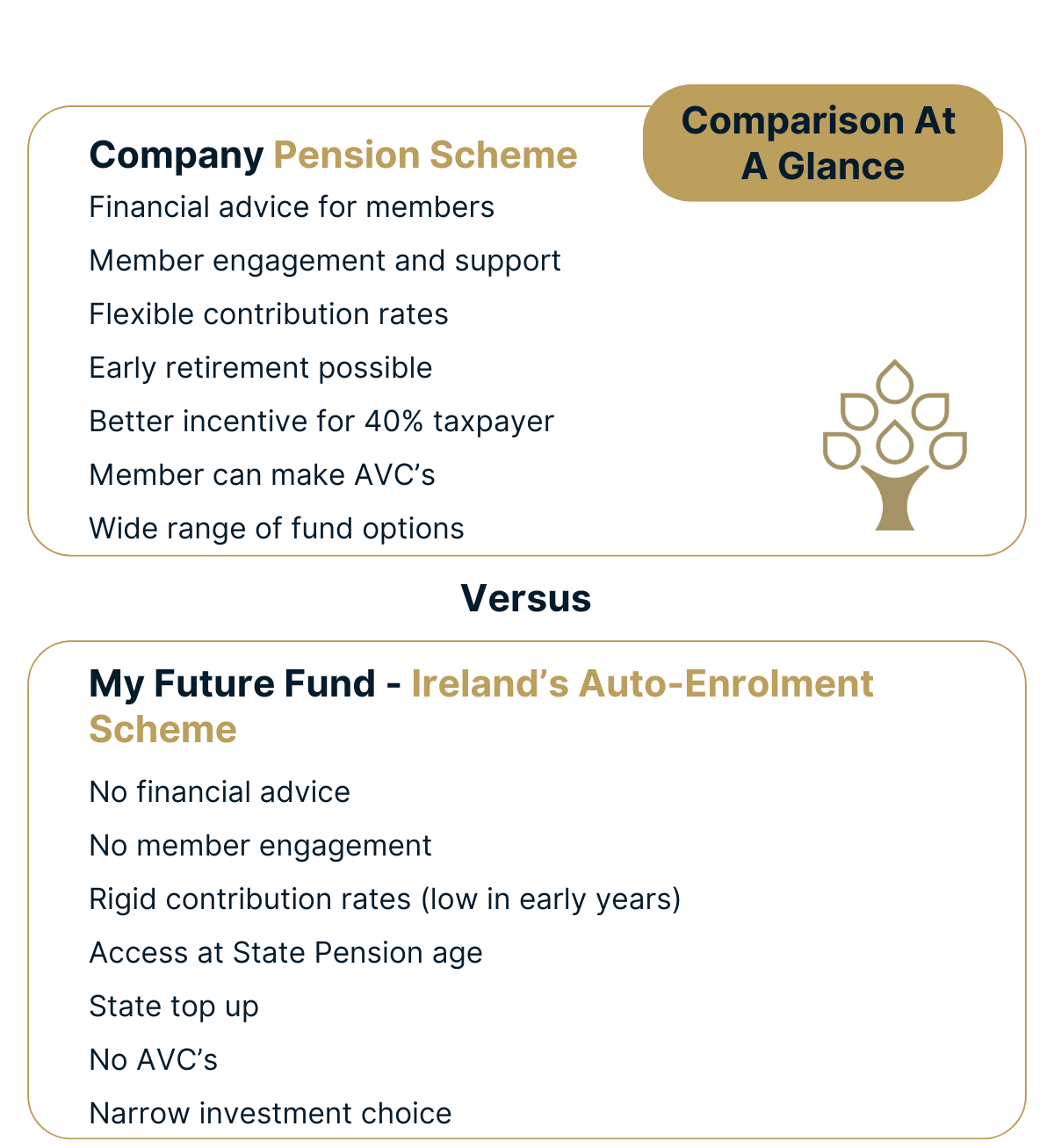

Auto-Enrolment marks a major step forward in retirement planning, especially for employees not currently saving. For some employers, particularly those with transient or lower-income workforces, it may become the default solution. When it is enforced, employers without an existing employee pension plan, will be facing a mandatory pension spend for the first time and will be required to make pension contributions in accordance with AE regulation. Tax incentives will differ between the government run system and the existing pension scheme system.

However, employers with existing private pension schemes have an opportunity to highlight the advantages of their own plans, such as higher contributions, better tax relief for higher earners, broader investment options, and access to professional advice. These schemes can also play a key role in recruitment and retention.

By acting now, you can establish a pension arrangement suited to your unique organisational needs, one that will allow you to create the single employee experience you want.

An overview of auto-enrolment.

Auto-Enrolment is a new retirement savings system for employees, proposed to come into effect in just a few months. Its aim is to make the decision to save for a pension easier for both employees and employers.

People will automatically be enrolled if they:

- Do not have a pension scheme.

- Earn more than €20,000 per year.

- Are aged between 23 and 60 years.

*People under 23 years and over 60 years may opt to be included

With regards to the income threshold, those earning less than €5,000 annually are not eligible to participate in the AE Scheme, while those earning between €5,000 and €20,000 can opt-in voluntarily but will not be automatically enrolled.

Auto-Enrolment scheme contributions.

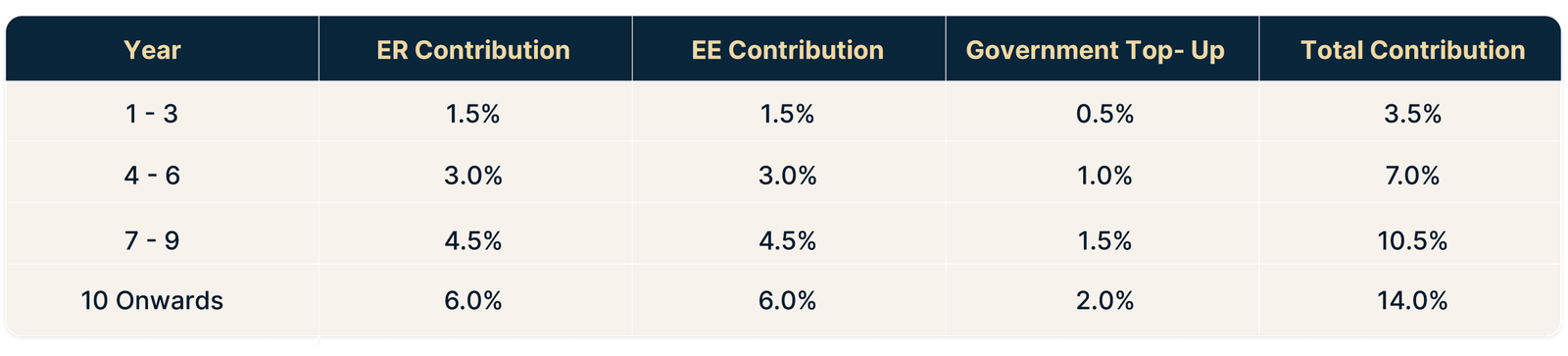

The contribution rates to the AE Scheme will include employee contributions, a matching employer contribution and a Government top-up equal to 1/3rd of the employee contribution. Contributions will increase every 3 years over the first 10 years of the scheme as seen the table below.

A key element of the AE Scheme is that these contributions are to be based on an employee’s total earnings including any fluctuating elements of pay that are taxable, for example, anything subject to Benefit In Kind (BIK) up to a maximum of €80,000 per annum.

The AE Scheme will work on the principle that all eligible employees will be included but they can at certain points opt out, pause or suspend their contributions after 6 months in the scheme. Where an employee opts out they will be enrolled back into the scheme after 2 years.

As the AE Scheme has yet to commence, it remains to be seen how onerous this will be for you as an employer or what impact it will have on your payroll to administer.

Why you need to act now.

Once your employees are auto-enrolled you are locked in to the mandatory contribution rates. By setting up your own scheme now, you maintain control over the costs associated with contributions.

Your employees will need to be part of a pension solution in advance of the start date of Auto-Enrolment (January 2026) as the National Automatic Enrolment Retirement Savings Authority (NAERSA) will:

- Look back over an employee’s payslips 13 weeks prior to the start date

- Ascertain if they are eligible to be included in Auto-Enrolment (the €5,000 rule)

Get ahead of the deadline and ensure you’re fully prepared with our free Auto-Enrolment guide

Benefits of a private pension scheme for all.

Control over costs

A private pension scheme allows you to set your own contribution rates for all staff, providing flexibility to design a plan that fits your company’s financial situation and your employees’ needs.

Staff acquisition

A private pension scheme can help you stand out to those in the job market, attracting a higher level of talent. AE reduces the differentiation between companies when comparing solely on pension offerings. It may require you to offer higher pension contributions or other additional perks.

Retention strategy

Many employees view a private scheme with favourable terms as a significant benefit, feeling more supported by their employer. This leads to increased loyalty, job satisfaction, and retention.

Future hires

AE will have a serious impact on Irish employers when planning future hires. Mandatory pension contributions will have to be calculated and will increase costs while also adding to the administrative burden and impacting budgeting. Having a private pension plan in place provides flexibility in structuring contributions, ensuring cost control while enhancing the overall compensation package.

Employee Retirement Services

Explore more employee benefit solutions.

Master Trust

Discover the ultimate solution for managing your employees' retirement savings effortlessly through a Master Trust Pension solution. Offering this pension solution demonstrates your commitment to employee financial wellness and to attract top talent. Additionally, Master Trusts simplify administration, offer tax benefits, and empower your workforce to take control of their retirement planning.

Personal Retirement Savings Accounts (PRSAs)

Currently, the only legal obligation on you is to offer your employees access to a Pension Solution. As Ireland's simplest pension option, PRSAs meet your legal requirements effortlessly. With recent legislative updates, PRSAs now offer enticing tax benefits and investment diversity, ideal for ambitious business owners and senior professionals planning their retirement journey.

Auto-Enrolemen: Frequently asked questions

If you need help evaluating your pension solutions, our experts are here to provide expert guidance and support every step of the way.

Employers must facilitate the Auto-Enrolment (AE) Scheme and inform employees when they have been enrolled, manage payroll deductions, and ensure compliance with contribution payment timelines.

Employees aged 23–60 earning over €20,000 annually and not already in a pension scheme will be automatically enrolled.

Contributions start at 1.5% of gross taxable earnings and increase to 6% over a 10-year period, matching employee contributions.

Yes, but only between months 7 and 8 after enrolment, and 6 months after each contribution increase. Employees will be automatically re-enrolled every two years.

Payroll systems must be capable of managing employee and employer contributions, and reporting to the National Automatic Enrolment Retirement Savings Authority (NAERSA).

If the employee is a member of an existing plan facilitated through payroll deduction, the employee will not be auto-enrolled. Employers must assess eligibility of existing arrangements carefully.

Yes. Employers may face fines or enforcement actions if they fail to enrol eligible employees or remit contributions properly.

The €80,000 threshold for contributions refers to gross pay earned in a calendar year. Once an employee has reached the €80,000 gross pay threshold in a given year, they will cease to make contributions on earnings after the pay period in which the threshold is breached. This means that there will be scenarios where contributions (both employer and employee) are paid on gross pay above €80,000. The example below shows how contributions will be paid on gross pay above €80,000.

Example

An employee paid monthly, reaches €79,500 annual gross pay to date in September.

The next payroll submission shows their gross pay to be €2,000 in October.

Their annual gross pay-to-date is now €81,500.

NAERSA will take and invest the employer and employee contributions on the €2,000 gross pay reported in October.

NAERSA will create a new AEPN at this point which will be available in payroll for the next pay run.

The new AEPN will include a contribution rate of 0% so that no further contributions are to be paid in that calendar year.

When the new calendar year starts a new AEPN will be available in payroll with the prevailing contribution rate to be applied.

There will be no refunds on the contributions paid on the €1,500 above the €80,000 gross pay threshold.

NAERSA and the Department of Social Protection will provide guidance, templates, and technical support for implementation.

The auto-enrolment scheme will be supervised by the Pensions Authority. It will have statutory independence and will be governed by a Board of Directors.

The Financial Services and Pensions Ombudsman services will also be available to participants.

Yes. Employers may continue offering occupational pensions which may have advantages for employees over the AE scheme.

Clear, proactive communication is essential. Employers should explain eligibility, contribution rates, opt-out rules, and long-term benefits.

Start your journey with solutions specific to your needs.

Whether you’re ready to schedule a time to talk or you’re interested in learning more about our services, feel free to fill out our contact form and we’ll be in touch.

Our Associations

- © Trust Matters Financial Planning. All rights reserved.

- Mamcol Limited t/a Trust Matters is regulated by the Central Bank of Ireland.

Mamcol Limited. Registered in Ireland No: 564942. Registered office: The Taney Buildings, 3 Eglinton Terrace, Dundrum, Dublin 14, D14 T9V0.